With the November 17 deadline looming, investors are, once again, contending with U.S. government shutdown risks. A newly elected House Speaker reduces those risks, and even if a shutdown occurs, we would expect a short-lived episode lasting no more than a few weeks. We see limited financial market impacts as likely, with risk of more acute headwinds if the standoff extends longer than expected.

In September, Congress passed a last-minute continuing resolution (CR) to temporarily avert a government shutdown. Passage of that CR ultimately led to the removal of former House Speaker McCarthy. With newly elected House Speaker Johnson proposing another CR, it looks unlikely that a shutdown will occur on November 17th. Instead, we expect an extension that pushes out the debate until January or April of next year. However, it is not a done deal, and Speaker Johnson seeking budgetary concessions to go along with military support to Israel potentially tees up a more partisan divide that could complicate the outcome of future negotiations. If a shutdown does occur, we would expect it to be short lived as political pressure to reach a deal is likely to be amplified by a shaky geopolitical backdrop.

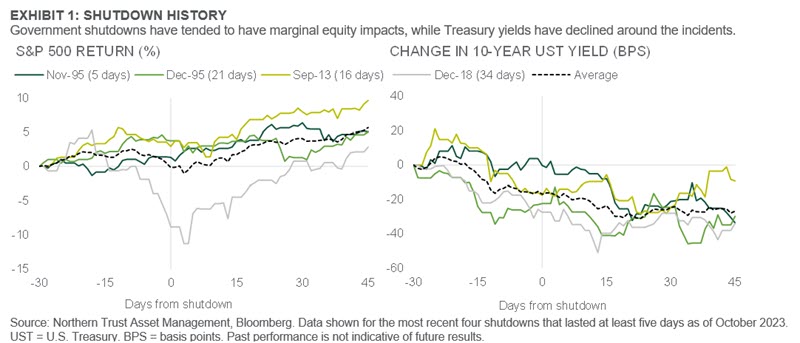

Overall, we expect a contained financial market impact under our base case of a shutdown lasting no more than a few weeks (if at all), noting risk of more acute headwinds to sentiment if the standoff prolongs. On average, recent shutdowns did not materially weigh on equities, while interest rates moved lower into the standoffs and thereafter (see Exhibit 1, which shows the most recent four shutdowns lasting more than a few days). Given today’s backdrop, we expect broader macro and central bank developments to be the more central driving factors.

Since 1978, there have been 16 government shutdowns lasting an average of eight days. The most recent one in 2018 happened to be the longest (34 days), however it was a partial shutdown and most of the federal government’s functions were unimpacted (including defense). The economic impact has tended to be modest and short lived. The 2018 episode shaved a few percentage points off of quarterly real Gross Domestic Product (GDP), which was recovered in subsequent quarters. Most estimates project a 1-2% hit to quarterly GDP if a month-long full shutdown were to occur today, with most of the lost economic growth likely to be recovered thereafter. A longer shutdown could decrease GDP growth more acutely due to furloughed workers and broader headwinds to consumer confidence.

We believe a shutdown would lower the odds that the Fed hikes its policy rate in December. While not all government agencies would fully cease activity (e.g., essential services continue), a shutdown could disrupt the production of key economic data produced by government agencies. This includes reports on employment and Consumer Price Index. The Fed is unlikely to make major changes in the absence of such data, seemingly adding to reason to keep its policy rate on hold. However, while rare, we note that the Fed has adjusted rates during shutdowns before, so a move would not be fully off the table.

Beyond potential disruption to the flow of key economic data, we are monitoring several other shutdown-related risks. In 2011, S&P downgraded its long-term credit rating of U.S. debt to AA+. Earlier this year, Fitch followed suit. Moody’s has indicated it may do the same should a shutdown occur this year, citing political polarization and broader risks on debt affordability from higher interest rates. Across the two weeks surrounding prior downgrades (in 2011 and 2023), U.S. equities lost 9.7% (2011) and 0.8% (2023). We don’t expect a Moody’s downgrade would be a major equity market headwind this time around, but we believe it is worth monitoring. We also note an incremental step-up in fiscal headwind risk if Congress does not agree on full-year appropriation bills for fiscal years 2024 and 2025. The Fiscal Responsibility Act (FRA) was enacted this June to temporarily suspend the debt ceiling. Housed within the FRA is language that would trigger automatic budget cuts if Congress is funding the government through stop-gap CRs past April of 2024. While this suggests a decent amount of time to pass the 12 appropriation bills, talks have made little progress so far and we believe the risk is worth monitoring.

CONCLUSION: SHUTDOWN RISKS DOWN BUT NOT OUT

Matters in Washington, D.C. are notoriously difficult to predict, though recent developments point toward a near-term government shutdown being less likely. In a letter to colleagues, House Speaker Johnson proposed passing another CR to fund the government through early 2024. Doing so would buy the House time to sign the essential appropriation bills to avoid a shutdown. Congress is likely keen to get back to work after three weeks at a standstill and with urgent funding issues requiring assistance. Although, while a CR looks likely, Speaker Johnson is known to hold strong conservative views regarding fiscal spending. Seeing all appropriation bills through the finish line could be challenging given Johnson’s views and a narrowly-divided House of Representatives.

Special thanks to Hunter Hildebrand, Rotational Development Associate, for data research.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A.

IMPORTANT INFORMATION. For Asia-Pacific markets, this information is directed to institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. The information is not intended for distribution or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. Northern Trust and its affiliates may have positions in and may effect transactions in the markets, contracts and related investments different than described in this information. This information is obtained from sources believed to be reliable, and its accuracy and completeness are not guaranteed. Information does not constitute a recommendation of any investment strategy, is not intended as investment advice and does not take into account all the circumstances of each investor. Opinions and forecasts discussed are those of the author, do not necessarily reflect the views of Northern Trust and are subject to change without notice.

This report is provided for informational purposes only and is not intended to be, and should not be construed as, an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Recipients should not rely upon this information as a substitute for obtaining specific legal or tax advice from their own professional legal or tax advisors. Information is subject to change based on market or other conditions.

All securities investing and trading activities risk the loss of capital. Each portfolio is subject to substantial risks including market risks, strategy risks, adviser risk and risks with respect to its investment in other structures. There can be no assurance that any portfolio investment objectives will be achieved, or that any investment will achieve profits or avoid incurring substantial losses. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Risk controls and models do not promise any level of performance or guarantee against loss of principal. Any discussion of risk management is intended to describe Northern Trust’s efforts to monitor and manage risk but does not imply low risk.

Past performance is not guarantee of future results. Performance returns and the principal value of an investment will fluctuate. Performance returns contained herein are subject to revision by Northern Trust. Comparative indices shown are provided as an indication of the performance of a particular segment of the capital markets and/or alternative strategies in general. Index performance returns do not reflect any management fees, transaction costs or expenses. It is not possible to invest directly in any index. Net performance returns are reduced by investment management fees and other expenses relating to the management of the account. Gross performance returns contained herein include reinvestment of dividends and other earnings, transaction costs, and all fees and expenses other than investment management fees, unless indicated otherwise. For additional information on fees, please refer to Part 2a of the Form ADV or consult a Northern Trust representative.

Forward-looking statements and assumptions are Northern Trust’s current estimates or expectations of future events or future results based upon proprietary research and should not be construed as an estimate or promise of results that a portfolio may achieve. Actual results could differ materially from the results indicated by this information.

Northern Trust Asset Management is composed of Northern Trust Investments, Inc. Northern Trust Global Investments Limited, Northern Trust Fund Managers (Ireland) Limited, Northern Trust Global Investments Japan, K.K, NT Global Advisors, Inc., 50 South Capital Advisors, LLC, Northern Trust Asset Management Australia Pty Ltd, and investment personnel of The Northern Trust Company of Hong Kong Limited and The Northern Trust Company.